Input to your Strategy for Adapting to Challenges

Feel free to pass on to friends and clients wanting independent economic commentary

ISSN: 2703-2825

23 July 2026

Sign up for free at www.tonyalexander.nz

Inflation should be lower

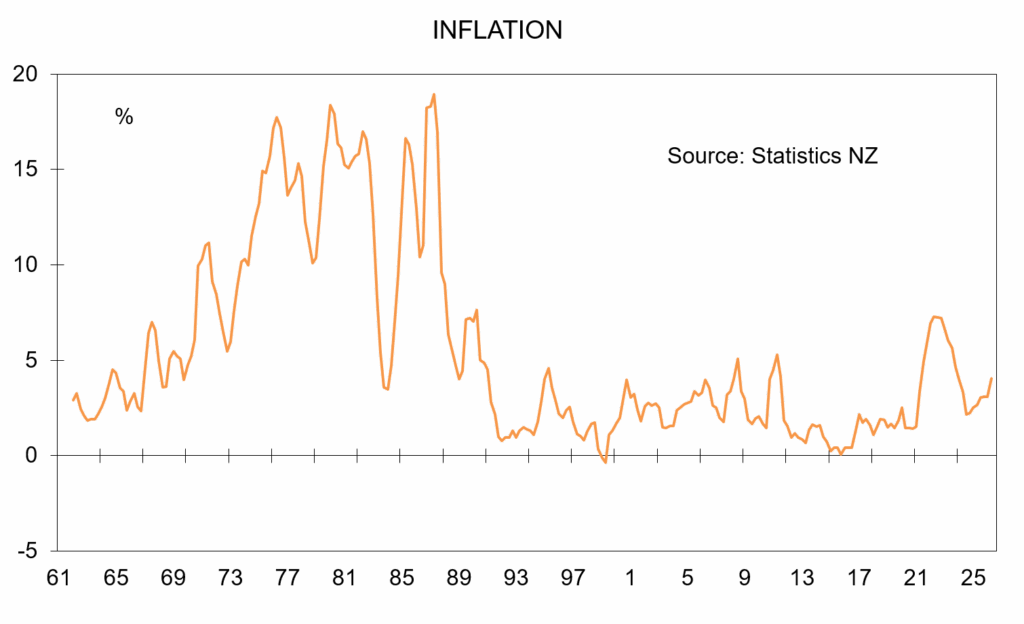

This week’s data highlight in New Zealand was the June quarter Consumers Price Index release by Statistics NZ on Tuesday. As had largely been expected inflation was 1.5% for the quarter and 4.1% for the year compared with 3.1% for the March quarter on a year ago and 2.7% a year back.

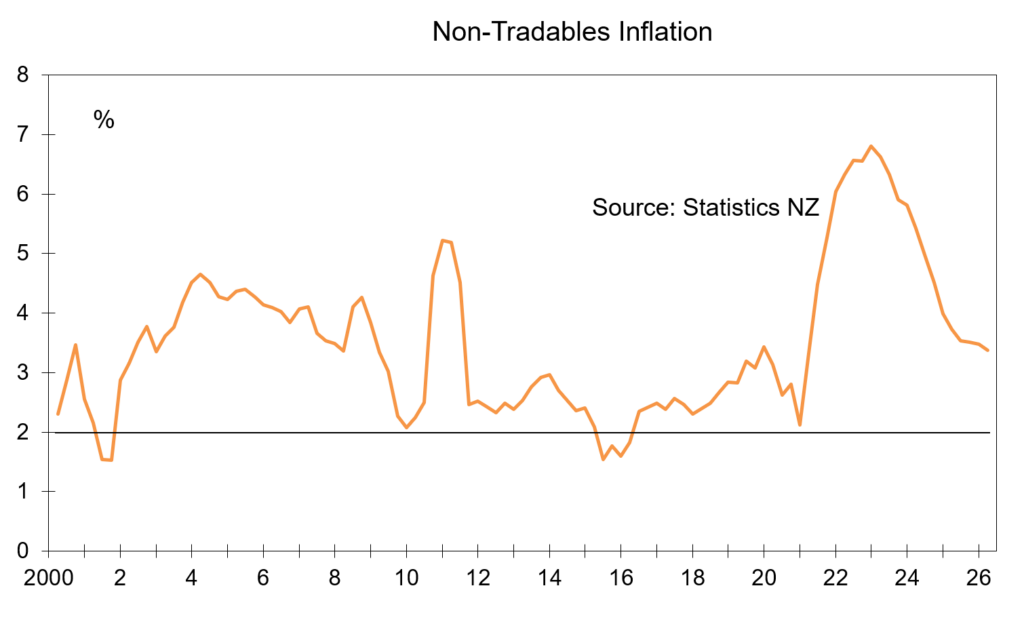

What really matters from the point of view of gauging inflation and interest rate risk is how underlying inflation is tracking rather than the headline number.

For instance, because of soaring fuel prices inflation for the quarter was boosted an extra 1% from what would otherwise have been a fairly good 0.5%. But I like to keep an eye on the non-tradeables inflation rate which excludes prices of things traded across the border.

On average since 2000 this inflation rate with a domestic focus has been 3.5%. It is now 3.4%. This is too high. One would hope that at the start of an economic upturn which will eventually boost inflationary pressures that this measure was starting the cycle at around 2.5%. The fact it is starting much higher than that means the risk of high inflation early on once the economic growth period returns for us is quite high.

In fact the situation is a tad worse than this because New Zealand’s accruing poor productivity performance means that for any given rate of growth in our economy inflation will now appear earlier than in previous years. Then it gets worse because a lot of inflation is coming in areas immune to monetary policy shifts – for example council rates and electricity prices.

This doesn’t mean the Reserve Bank are about to hike interest rates tremendously. But they have indicated recently that they are concerned about how high inflation has been and the risk of businesses eventually being in a position where they can increase their selling prices and get away with it.

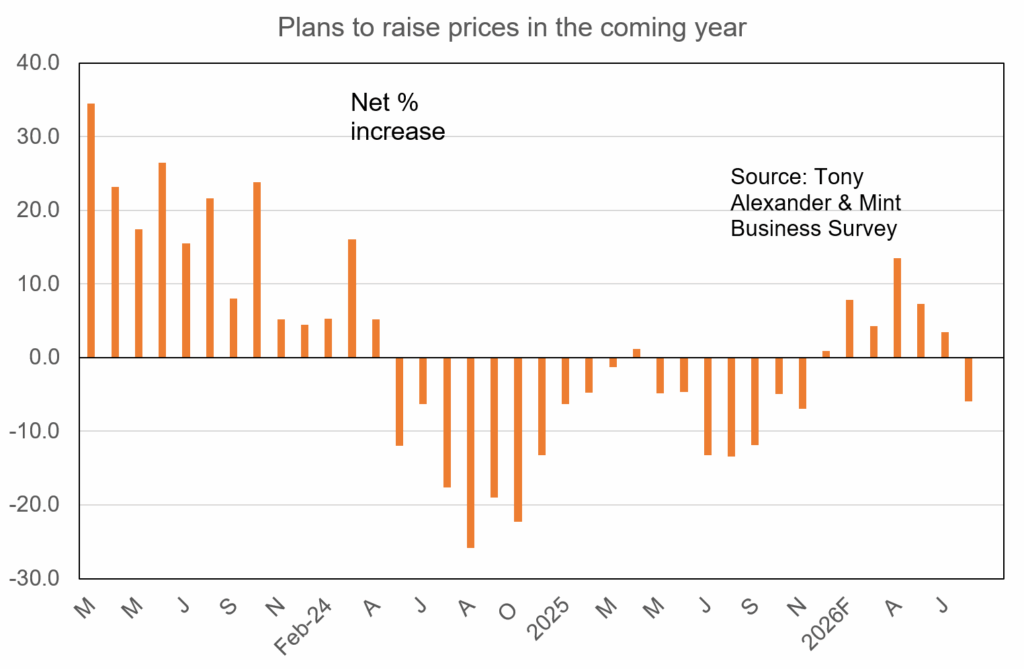

We are not at that point yet as evidenced by the results of my Business Survey with Mint design people sent out earlier this week. A net 6% of respondents have indicated that they do not intend raising their selling prices over the coming 12 months.

This accords with comments from businesspeople that their margins are crunched and they would like to raise their prices, but conditions are too competitive currently and they feel they cannot do it.

Come the next cash rate review in early September another 0.25% cash rate increase is highly likely with another to follow late in October. After that discussion will centre around how long a pause if any the Reserve Bank will take to see how much extra restraint will need to be applied.

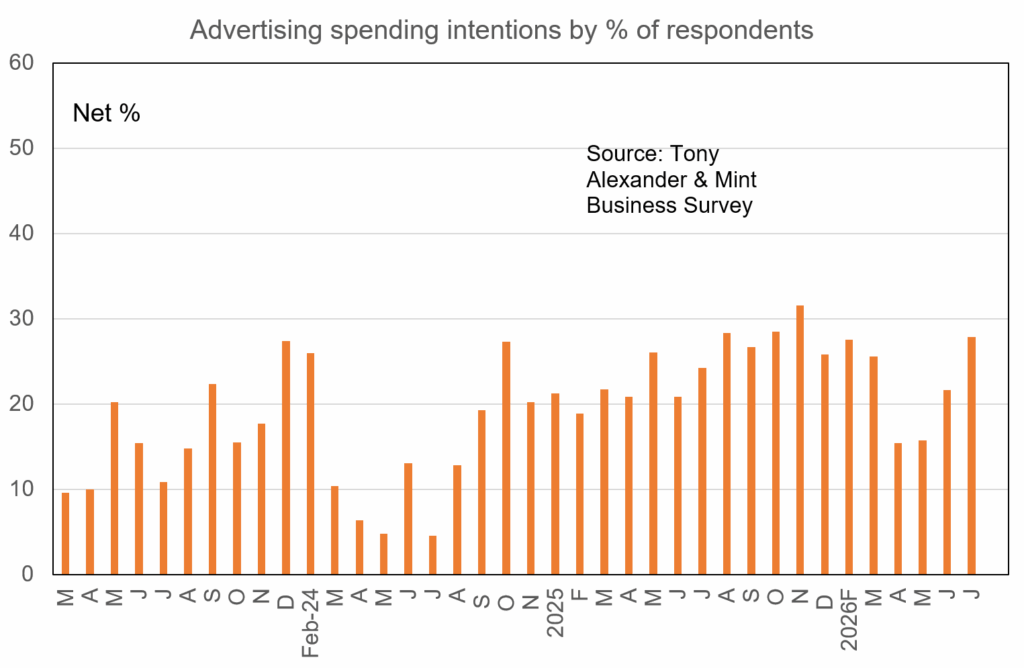

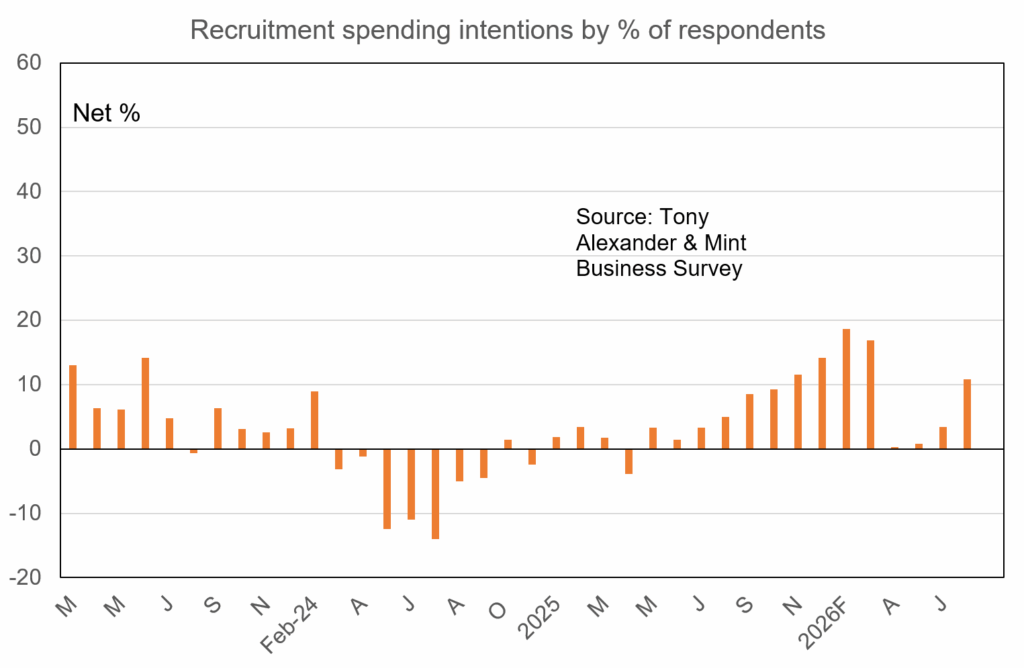

Just another couple of things worth highlighting from my business survey are the upward movements in plans for spending on advertising and recruitment. These indications bode well for the resumption of growth in our economy once the current oil price spike fades into the rearview mirror.

Trouble is we don’t know when that will be, especially as this time around global oil stocks in reserve are much lower than on February 28 and shortage risks therefore are greater – along with upside potential for petrol and diesel prices. Good luck to all of us.

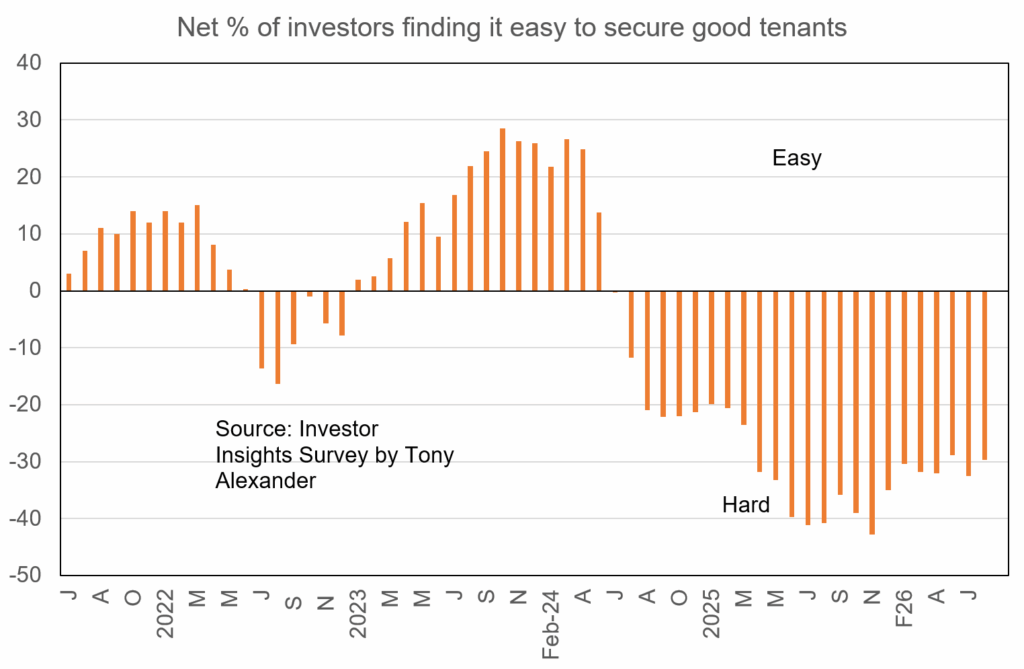

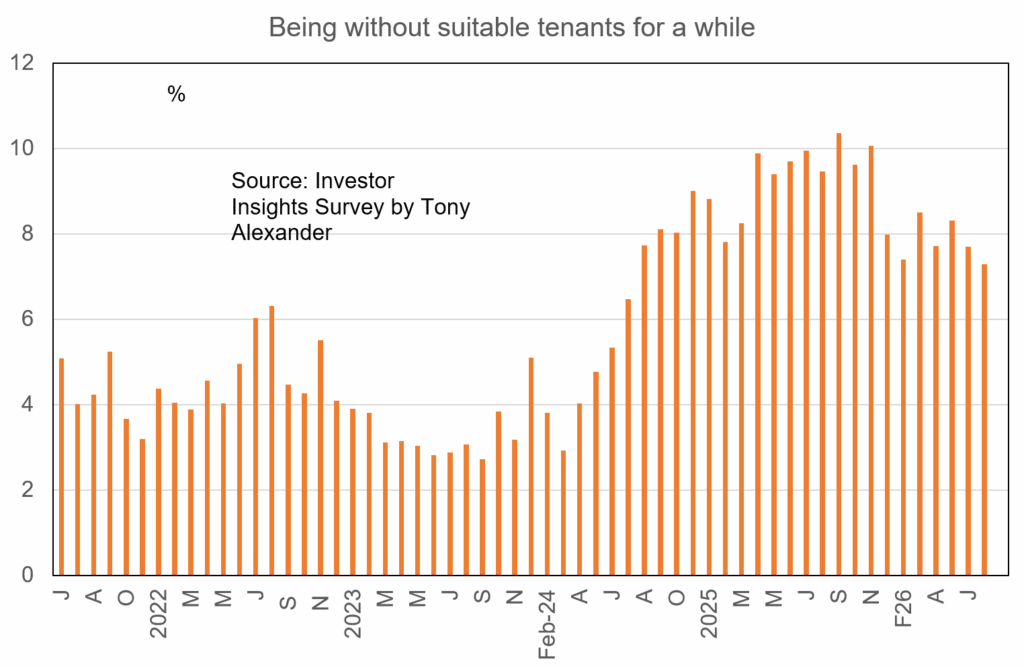

Something else worth highlighting comes from my monthly survey of residential property investors, now newly sponsored by The Property Consortium Ltd.

For the first time we asked investors which region they think may be best for buying an investment property in the coming year. 26% opted for Canterbury even though the region only accounts for about 13% of the country’s population.

This likely reflects the well known good affordability of Christchurch property compared with Auckland and Wellington in particular along with the greater economic strength and recent house price performance for the region than most other parts of the country recently.

6% chose Southland and 11% Queenstown Lakes District. Wellington region with under 11% of New Zealand’s population attracted just 7% of respondents. Auckland at 34% attracted 30% support so there or thereabouts.

Finally, it is worth noting that while overall landlords still firmly note that it is harder than usual to get a good tenant, the degree of difficulty seems to be slowly easing off.

This is backed up by a decline underway in the proportion of landlords saying that they are concerned about being without a tenant for a while.

If I were a borrower, what would I do?

This week’s inflation number was largely as expected at 4.1% so had little impact on wholesale interest rates. But the general drift for the week has been slightly upward on the back of slightly higher rates offshore mainly associated with increases in energy prices.

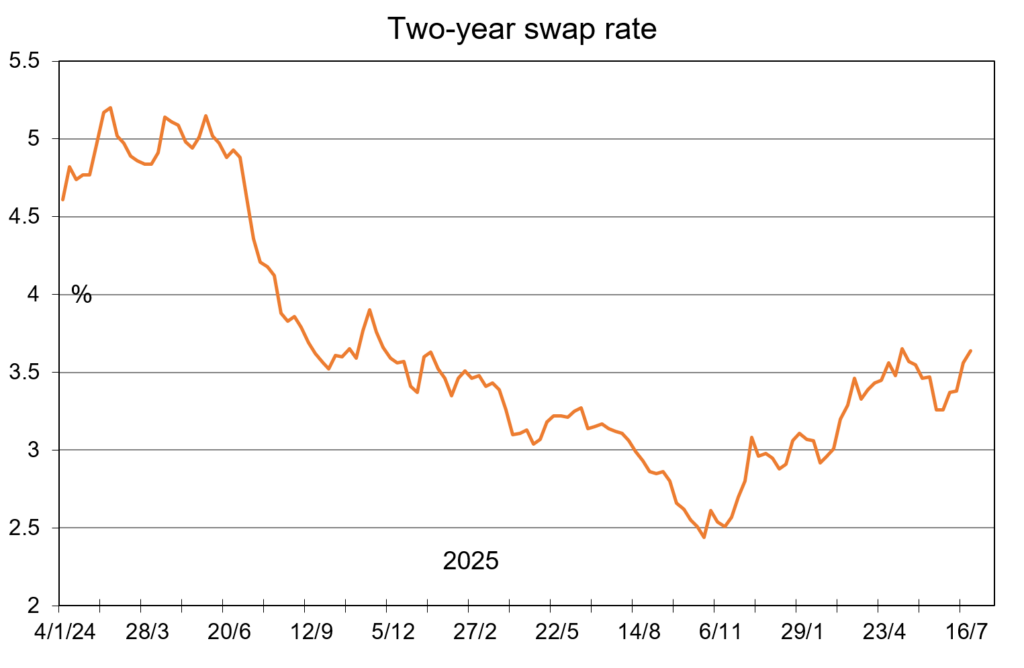

The two year swap rate relevant to the cost of funds for banks lending at a fixed two year rate has moved up to near 3.64% from 3.56% last week and 3.26% four weeks ago.

It is very clear that interest rates are rising and that includes mortgage rates. But the timing of fixed rate rises can never accurately be predicted as it depends on whether or not banks wish to try and grab or protect market share.

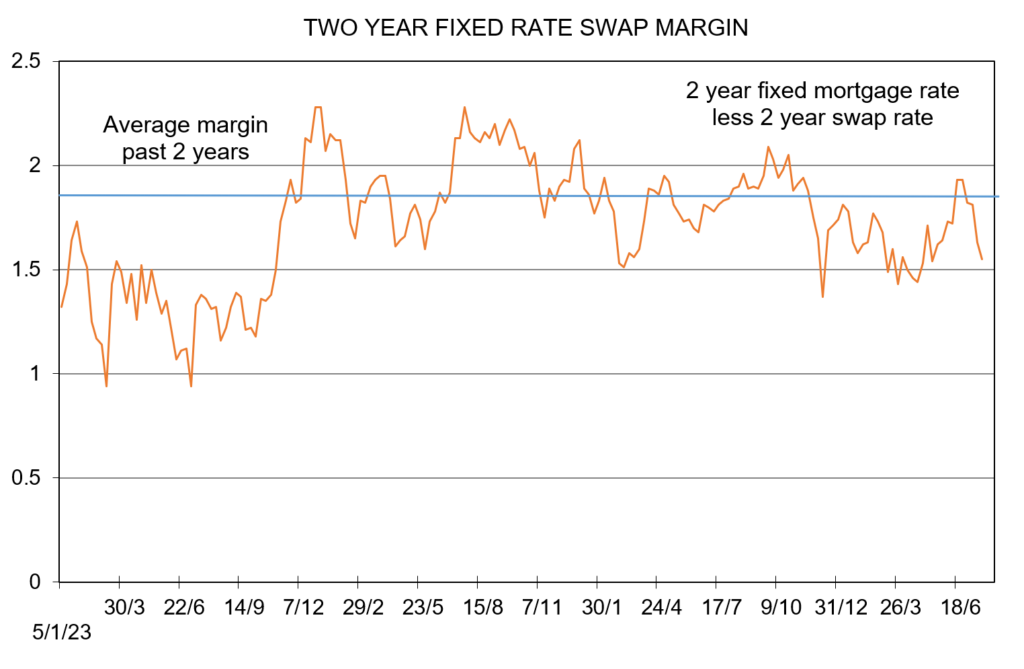

However, pressure is on them for another round of rate rises with margins running below average levels.

If I were borrowing at the moment, I would still favour fixing three years.

Nothing I write here or anywhere else in this publication is intended to be personal advice. You should discuss your financing options with a professional.